Middle East tensions rattle global energy supply chains, with African exporters and importers facing mixed economic fallout

Kemi Osukoya

G7 & MARKETS

Energy markets and the global economy are bracing for another shock.

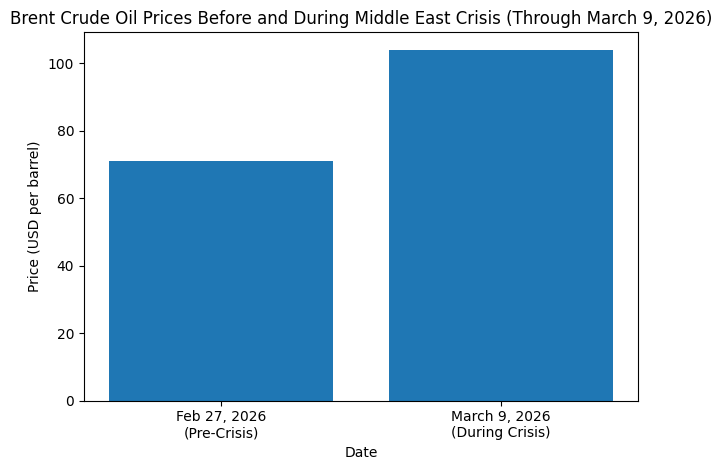

Finance ministers from the Group of Seven signaled Monday they are prepared to intervene in oil markets as conflict in the Middle East threatens global energy supply and sends prices toward the psychologically important $100-per-barrel mark.

Meeting virtually with leaders from the International Monetary Fund, World Bank Group, Organisation for Economic Co‑operation and Development and the International Energy Agency, ministers discussed the impact of the conflict on financial markets, global trade routes and energy flows. Officials said they stand ready to take “necessary measures,” including a coordinated release of emergency oil reserves, if supply disruptions intensify.

The warning comes as the Strait of Hormuz—one of the world’s most critical oil shipping lanes—remains under pressure from regional conflict involving Iran, threatening to choke off a significant share of global crude exports. Oil prices were trading around $100 a barrel early Monday, but policymakers fear the conflict could quickly push prices above $100 if supply routes remain constrained.

President Trump said in a Truth Social post on Sunday that “short term oil pricers, which will drop rapidly when the destruction of the Iran nuclear threat is over, is a very small price to pay for U.S.A and the World Safety.”

The International Energy Agency‘s chief Faith Birol and other officials say the oil market has deteriorated in recent months, creating “significant and growing risks” for global energy supply. One option under discussion is a coordinated release of as much as 300–400 million barrels from strategic reserves held by major economies—roughly a quarter of the emergency stockpile maintained by industrialized countries.

For African economies, the implications are significant. Oil-exporting countries such as Nigeria and Angola could benefit from higher crude prices, boosting government revenues and foreign exchange inflows. But for large energy importers—including Kenya, Ghana and South Africa—a sustained price spike risks fueling inflation, widening trade deficits and increasing pressure on already fragile currencies.

Beyond energy markets, the G7 discussions also touched on broader economic coordination, including safeguarding global supply chains, strengthening partnerships with developing economies and mobilizing financing through multilateral institutions. For African policymakers, the latest global developments once again underscore how geopolitical shocks far beyond the continent can quickly ripple through domestic economies—affecting everything from fuel prices and transport costs to food inflation and fiscal stability.

Across Africa, the economic ripple effects of the Middle East crisis are already showing up in trade flows and export markets.

For many African economies, the Gulf and wider Middle East remain critical commercial partners, serving as both major import markets and logistical hubs for global distribution. The disruption has begun to slow that pipeline. In Kenya, for instance, a significant share of the country’s tea exports is routed through Dubai in the United Arab Emirates, one of the region’s largest commodity trading centers. With supply chains under strain and regional uncertainty mounting, exporters say shipments of agricultural products—including tea, meat and fresh produce—have slowed or temporarily paused.

South African Foreign Minister Ronald Lamola also warned of disruption and negative impact on the South African economy and the wider continent, noting that the instability in the Middle East risk widening the conflict with grave implications for regional and international peace and security as well as economic costs.

The interruption is forcing governments and exporters across the continent to look for alternative markets and trade routes, but the shift will take time. For now, governments and many businesses are bracing for short-term revenue losses as logistics networks adjust and buyers in the Middle East reassess demand amid the instability.

The stakes are high. Beyond energy markets, the Middle East has become an increasingly important destination for African food exports, aviation links and investment flows over the past decade. Any prolonged disruption could squeeze exporters already navigating volatile currencies, rising transport costs and tighter global financing conditions. For African economies deeply integrated into Gulf trade networks, the conflict is quickly becoming not just a geopolitical crisis, but a commercial one.

With energy markets on edge and key shipping routes under strain, energy ministers from the G7 are expected to meet virtually Tuesday to weigh the next steps to stabilize global oil supplies. The talks come as geopolitical tensions in the Middle East raise fears of a broader market disruption that could deliver the next major shock to the global economy, once again testing the resilience of emerging markets across Africa.