Its resilience depends on how quickly finance ministers and central bankers can adapt and mitigate shocks

Kemi Osukoya

GLOBAL ECONOMY

At the headquarters of the International Monetary Fund in Washington D.C, there was little pretense this week—no soft framing, no bureaucratic hedging. Just a stark message from Managing Director Kristalina Georgieva: the global economy, once again, is being stress-tested—and this time, the shocks are converging.

“A resilient world economy is being tested again,” the Managing Director said, opening the IMF’s curtain-raiser ahead of next’s IMF/World Bank Spring Meetings. The now-paused war in the Middle East, she added, has already rippled far beyond the region, delivering what she described as a classic and punishing negative supply shock.

This is not a theoretical exercise. It’s a triple shock, one system that is already playing out in energy markets, food systems, and capital flows—with consequences that will define the near-term trajectory of global growth.

At the heart of Georgieva’s warning is a three-channel disruption: energy, supply chains, and food security. The numbers alone tell a sobering story.

Global oil flows dropped by roughly 13%, while LNG flows fell by about 20%. Brent crude surged from $72 per barrel before hostilities to above $100. While prices have since eased, it remain structurally elevated—at $96.92 a barrel early Thursday, forcing countries to pay premiums for access to already strained supply.

“This requires understanding the nature of the shock… the size of the impact, and the policies that can mitigate it,” she remarked.

The shock is not evenly distributed, she noted, underscoring it is global in reach but asymmetric in impact. Energy exporters such as the U.S., Russia and those in Africa-Nigeria, Angola with stable output are better positioned. Import-dependent economies—particularly in Sub-Saharan Africa and small island states, on the other hand are absorbing the heaviest blows, often with limited fiscal space to respond. And then there are the second-order effects: refinery disruptions, shortages of diesel and jet fuel, and cascading supply chain breakdowns—from fertilizers to semiconductors.

Food insecurity alone is expected to push an additional 45 million people into hunger, bringing the global total to over 360 million, according to United Nations Food and Agriculture Organization and the World Food Program.

For central bankers, the risk is not just inflation—it is inflation expectations, the IMF chief stated.

The first channel is mechanical: higher input costs feed directly into consumer prices, dampening demand. The second is more dangerous. “These can break anchor and ignite a costly inflation process,” Georgieva warned. “Been there, seen it.”

In other word, it’s inflation second act.

So far so good, long-term inflation expectations remain stable—a critical buffer. But the margin for error is also narrowing. Financial conditions, meanwhile, have already tightened. Emerging market spreads have widened, equities have adjusted, and the dollar has strengthened—though some easing has recently emerged.

She noted the policy dilemma for central bankers and finance ministers is familiar but no less fraught: act too soon, growth is crushed; act too late, risk an inflation spiral.

Even under the IMF’s most optimistic scenario—one that assumes a relatively swift normalization—global growth is set to be revised downward in the forthcoming World Economic Outlook.

Why? Because the damage from the Middle East crisis is already embedded, she stated in her remarks.

Infrastructure losses, disrupted supply chains, and weakened confidence are not easily reversed. Georgieva pointed to Qatar’s Ras Laffan LNG complex—responsible for 93% of Gulf LNG output—as a case in point. Shut down since early March and directly hit days later, it could take up to five years to fully restore capacity.

And there will be no clean return to pre-crisis conditions, she warns.

“We don’t truly know what the future holds,” she said, referencing continued disruptions in critical maritime routes like the Bab-el-Mandeb Strait. “What we do know is that growth will be slower—even if the new peace is durable.”

Her policy prescription: Do no harm.

“This being a classic negative supply shock, demand adjustment is unavoidable,” Georgieva said plainly. “We can’t go through this without some pain.”

But policymakers can make that pain manageable—or more worse, she noted, underscoring restraint.

Her warning against “go-it-alone actions”—export bans, price controls, and broad subsidies—was unequivocal: “Don’t pour gasoline on the fire.” Instead, the playbook should be disciplined and targeted: Central banks should remain vigilant, prepared to tighten policy if inflation expectations begin to slip, but otherwise guided by incoming data. Fiscal authorities, for their part, are urged to focus on targeted and temporary support for vulnerable households and firms, avoiding broad-based measures that strain already stretched public finances.

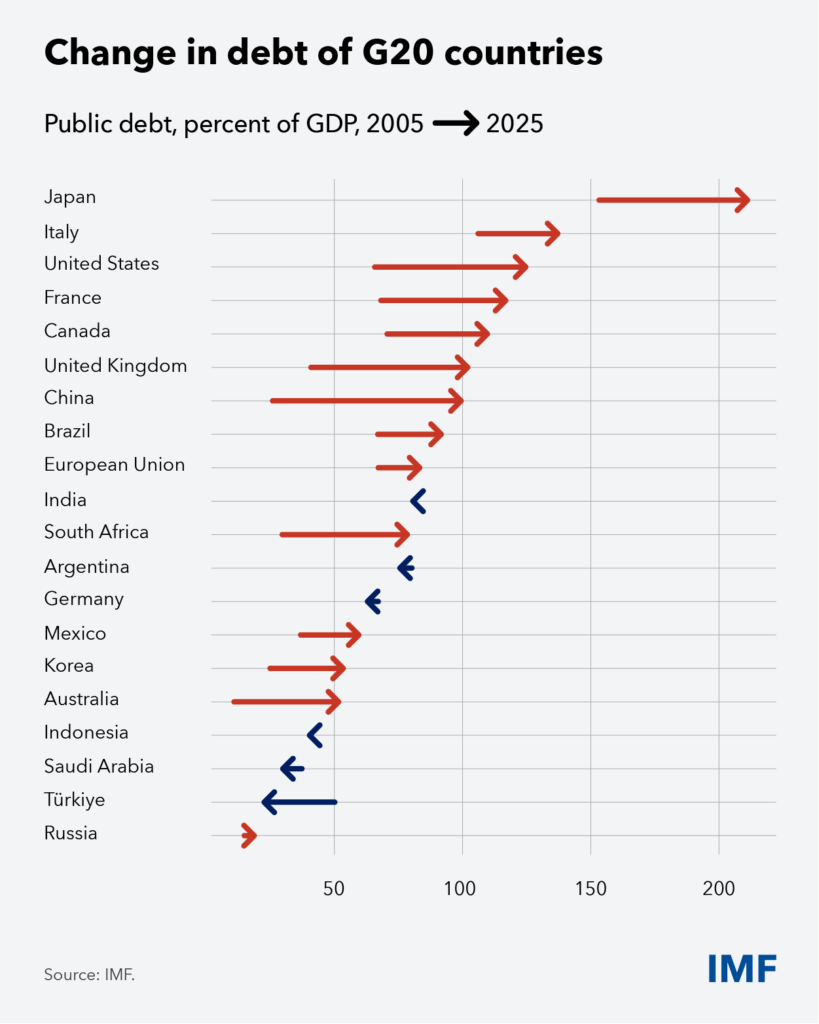

That constraint is becoming increasingly binding. Public debt levels across much of the world are significantly higher than they were two decades ago, while rising interest rates are pushing up the cost of servicing that debt. The result, Georgieva warned, is a shrinking margin for policy maneuver. Stimulus financed by additional borrowing could intensify financial tightening, leaving governments caught between competing objectives.

“It would be like driving with one foot on the accelerator and the other on the brake—not good,” she said.

And yet, for all the caution, there is a through line of pragmatic optimism in the IMF chief’s message: “the most important message… is get your house in good order,” Georgieva said during the Q&A session of her speech. “When this shock dissipates, there will be another one to come.”

Resilience, she framed, is not about avoiding shocks—it is about preparing for them.

That means structural reform: removing barriers to private sector activity, investing in productivity, and enabling capital to flow efficiently. It also means recognizing the role of business itself.

“One of the reasons the world economy has shown so much resilience is because… the private sector is more agile, more adaptable,” she noted. “Remove red tape, remove obstacles to innovation… and on that basis, lift up productivity.”

There are precedents, she stated. Countries like Greece, Ireland, and Portugal were once at the epicenter of the eurozone crisis in the 2000s, but now have emerged as some of Europe’s stronger performers, precisely because they used crisis as a catalyst for reform.

Looking forward ahead, she noted that beyond the immediate shock lies a more structural transformation. A bigger shift in the global economy powered by artificial intelligence. AI-driven productivity gains could add between 0.1% and 0.8% to global growth, according to IMF estimates, potentially lifting the world economy above its pre-pandemic trajectory, she added. But that upside comes with labor disruption risks, she warned, particularly in advanced economies where up to 60% of jobs could be affected.

At the same time, the global economy is undergoing a broader realignment. Trade patterns are shifting, alliances are evolving and geopolitical tensions are reshaping supply chains, however, she rejected the notion that countries can insulate themselves entirely. “The one thing that is not possible is to pull yourself out of interdependence,” she said. “Even the largest economies cannot do that.”

She said trade shifts also bring new opportunities such as regional trade corridors. Case in point, she noted that while trade among European nations is 60%, within ASEAN countries, it is around 20%. “Why are these countries not trading more with each other?” she asked rhetorically before adding, “that is something that they’re reflecting on, and we would like to help them to build, not only more vibrant trade relations, but also to think about their collective strength and put it in place.”

Gulf countries were already working robustly on coordinating their reforms, improving their inter connectivity, until this war affected them. Africa, she said has so much potential in regional trade. “When you look at the continent of Africa, there is so much if you take problems as opportunity, many of those that comes with improving regional trade, regional integration, you take another angle, non tariff barriers.”

She said the Fund’s immediate priority is to ensure it has the capacity to respond to the crisis, insisting the institution is well positioned to meet that need of its members.